Where Crypto VC Goes From Here

The industry's path forward after its terrible, horrible, no good, very bad year

Setting the stage

Crypto has had a rocky twelve months. FTX facilitated the largest corporate fraud in recent history. A large number of centralized crypto lenders - once high flying unicorns - have gone bankrupt. In the process, prominent venture investors - Sequoia, Bain Capital Ventures, Canadian pension funds - have had large investments blow up in a spectacularly public fashion.

In poker you play your hand and you know in the span of a glass of whiskey whether you’re leaving with your chips. Venture capital is a game of much longer feedback cycles. It can take a decade to know whether you have a straight flush. Tokens compress these time scales, but these investments are still measured over years.

Crypto VC is at a crossroads. Most funds have put a good chunk of their chips on the table - few new funds have been raised in the last 6-9 months and so I think it is fair to assume that most funds are 30-70% deployed. At the same time, few 2021 and later vintage crypto VC funds have returned any meaningful capital to investors. Most managers are extending their deployment timelines but many will realistically have to raise in the next 12 months.

In this piece I try to dissect where we are in the cycle, what the next fundraising cycle may look like for managers, and what implications this will have for the markets. I conclude by exploring where opportunities may lie.

Crypto cycles often rhyme

2023 crypto feels a bit like 2019. We had a grand old time for 18 months and now we’re paying the price. In both cycles a speculative surge drove a huge amount of retail investor interest into the space. The catalysts were different - ICO’s in 2017, DeFi summer/NFT’s/stimmy checks in 2020. But the end result was structurally similar in that a huge amount of venture funding followed - and likely reinforced - retail inflows.

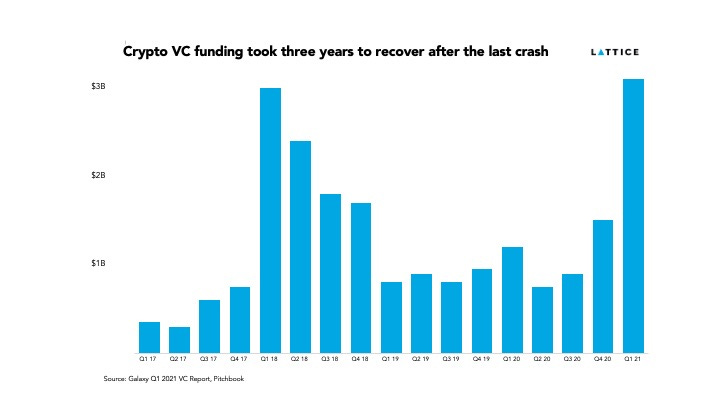

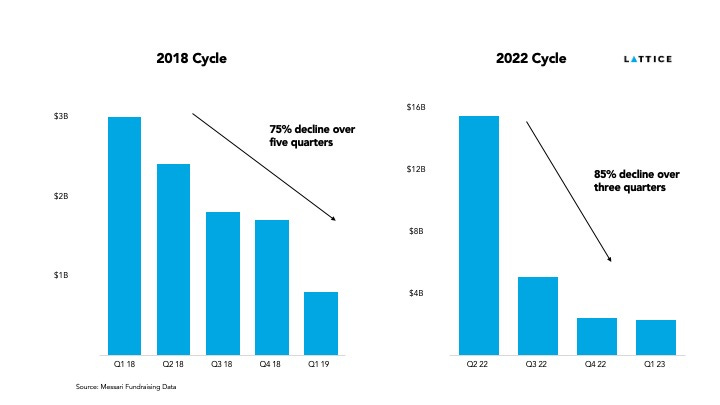

In the last cycle crypto VC funding started recovering after two years and took another year after that to fully bounce back (see appendix). That would mean we’re currently in 2018Q4/2019 Q1 territory - near the bottom of the cycle but with no immediate positive catalyst on the horizon. This intuitively feels right - I sense some apathy starting to set in and I haven’t heard any convincing cases on near term catalysts.

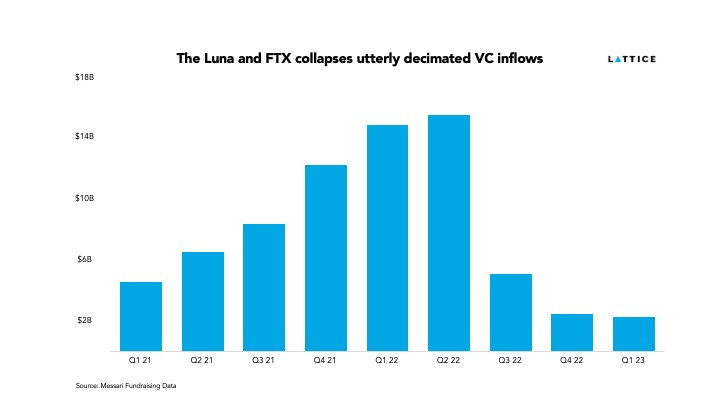

This cycle saw higher highs and a faster collapse than the last one. I don’t have perfect datasets to compare VC funding across cycles, but we almost certainly saw at least 2-4x more VC capital enter this time around. While 2018 saw a linear decrease in VC funding over a year, this cycle saw a sharp collapse after 2022 Q2. This shouldn't be surprising as this collapse was driven more by black swan events (Luna and FTX implosions) than last cycle’s slow decline.

This cycle is also clearly different from 2018 in important ways. Blockchain technology, use cases, and userbase have all increased by an order of magnitude. I’ll talk about that more later.

But the macro situation is objectively worse. Interest rates are rising, which generally decrease investment in VC broadly. There is also a huge amount of macroeconomic uncertainty. And VC faces the ‘denominator effect’ where some institutional LP’s find themselves over-allocated to venture due to declining equity prices. There are significantly more macro headwinds for managers than there were last cycle.

Managers Face a Chilly Reception

In the absence of actual returns data, fundraising becomes about telling a story. You highlight winners from your last funds and use a combination of anecdotal evidence and data to spin a story about financial outcomes. For example - we invested in ‘hypothetical DeFi company’s’ seed round - since then a16z led a Series A, meaning this well-executing team is now extremely well capitalized. We believe they’ll launch a token in the next 12 months which, based on market comps, could trade at a $1-2B FDV, giving us a 10-20x return on our initial investment. Something like that…

This story was easy to tell in 2021. Tokens launched and went up. Blockchain was the future. SBF was going to be the world’s first trillionaire. LP’s lapped it up - VC capital deployed into crypto (which can serve as a proxy for funds raised) exploded.

The story is harder to tell now. LP’s need to believe that real applications of blockchain technology emerge. And that these produce venture-scale outcomes. And that an aggressive SEC will not prevent US based venture funds from being able to access the best deals. I personally believe that all of these are true, but it’s clearly harder to make the case for this now than it was a year ago.

Now there is an alternative story to tell which is that you generally want to buy assets low and sell them high. There was clearly more hype in crypto around 2021, but that also meant that entry prices were higher. There is less hype now and so they are lower. I also believe this to be true. However, it’s a different story and my sense is that it's one that is harder for capital allocators to get onboard with.

My rough mental model is that most large capital allocators that invested in crypto VC over the past few years had 1-2 internal crypto champions. There were people at these institutions that started reading about crypto, got very interested in it, and started pushing it internally. They were not hired to do crypto and so still covered other asset classes, but they became the ‘crypto person’ at the firm.

My other rough mental model about these capital allocators is that they tend to be consensus driven (and often political). Most family offices have an investment committee that has to approve all investments. Endowments and pensions are structured similarly. Crypto is still relatively unproven and so naturally all of these institutions have a cohort of folks that are skeptical of it. And so whatever investments these firms made over the last few years, they were generally a result of the ‘crypto person’ at these firms being able to convince the rest of the firm to take a bet.

In 2021 the sector was hot and had produced absolutely insane returns and so the crypto person at most allocators did not have to expend that much political capital to get investments through. If crypto funds could produce 100x returns, investing in a fund that only delivered 10% of those returns would still be an excellent outcome. Hence, capital flowed into the space.

Today it’s not so fun to be the crypto person at a capital allocator. If you started investing in the space in 2020 or 2021 you probably have not made much money for your firm. And you’re now having to answer a ton of questions about FTX and Terra and Elizabeth Warren and the SEC. You like crypto but you like your job more and so you probably are spending more time on the other asset classes that you cover and not pushing crypto as much internally.

Implications of LP Pushback

Let’s assume that I’m right and there is an extended pullback in LP capital flowing into the space. What are the follow on effects?

Some funds get shuffled out

A lot of managers made (retrospectively) dumb decisions this cycle. If they can’t justify those decisions to their LP’s, those LP’s are unlikely to support a next fund. If their current LP’s are not going to re-up, it’s unlikely that new LP’s will support them. Every fund manager (us included) made decisions in the bull run that they wish they could take back - they bet on the wrong category, paid too high of a price, backed a team that is now pivoting out of crypto.

I don’t have proprietary knowledge of performance for most funds’ and so won’t speculate on who this impacts. There are probably sectors that look especially bad right now - growth investments, gaming, Polkadot. But tides change fast in this business and its totally possible that some or all of these categories are vindicated during the back half of this year.

I’d originally framed this section as ‘the bottom quartile gets shuffled out’ but I don’t think its that simple. I have heard first hand accounts of multiple ‘top’ crypto funds struggling to raise subsequent funds because performance data does not live up to external perceptions. Some top funds may have also scaled up too fast and won’t be able to rightsize.

The top quartile quietly quits

If a fund has been investing in crypto since 2019 or earlier, there is a good chance that the GP’s of said fund are quite rich. The fund has likely returned at least a few good vintages and they likely hold a good deal of low-cost-basis crypto in their PA’s. Money can buy fun distractions. A lot of crypto VC’s are into expensive sports - golf, kiteboarding, skiing. So you could do those things. Or you could jet between Mykonos and Miami splurging on bottle services. Or you could just spend time with your family.

Money is not distracting for everyone - I am consistently impressed with the work ethic of many very successful crypto VC’s. But its distracting for some number of people. And it gets more distracting when this job becomes less fun. This job is less fun in many ways than it was a year ago - you have more questions from your LP’s, you have to spend more time with lawyers, fundraising is harder.

So I think some percent of successful GP’s fade into the background. Some will try to turn over their funds to younger leadership. Some will convert their funds to family offices and return outside capital. Others will just mail it in until their LP’s stop supporting them.

Funds will (try to) right size

Sometimes funds get too large - they raise a large fund during a bull market and by the time they start deploying that capital six months later, they think the opportunity has shrunk and so they rightsize their funds. Sometimes funds decrease the size of their next fund. Sometimes they do this while they’re deploying. LP’s generally like this - it’s easier to multiply a smaller amount of money.

Founders Fund recently halved the size of their next flagship fund. Other top funds will likely follow. There is historical precedent for this in market downturns. Kleiner Perkins, CRV, and Battery Ventures all cut their funds by 25-50% after the dot com crash.

Downsizing has consequences - management fees, which are directly tied to how large a fund is, fund day-to-day operations. So funds often have to downsize their teams in response. And my assumption would be that team members often voluntarily depart as the signaling is not necessarily super positive. If you can join a new fund that does not have baggage that is forcing it to rightsize, that’s probably a pretty attractive option.

While it seems like this downsizing process can happen in an orderly fashion, my assumption is that it won’t amongst crypto VC’s. Crypto VC’s have grown their funds - and teams - really quickly. And this is crypto - things are rarely orderly in either direction.

Opportunities in Choppy Waters

These shifting winds will create space for new entrants. The market isn’t exactly zero sum, but funds leaving the space will create more market opportunity for newer funds to launch and build brands. I expect that a decent number of investors at established funds that have hit headwinds will venture out on their own.

This will also create opportunities for funds with more novel strategies. I think there’s a lot of room for new managers to focus on liquid tokens (see Pangea). If you can figure out LP redemptions in a bear market and handle the volatility, the risk/reward on the liquid side can definitely rival doing privates. There’s also a lot of new categories that upstart funds have carved out - see EV3 in DeWi or Cooper Turley in music NFT’s. It’s still too early to tell if these categories will produce venture scale outcomes, but the rewards will be large if they do. There’s also room for innovation on fund structure - just look at what Amit Mukherjee is doing at Chainforest.

Darkest Before the Dawn

Crypto VC funding is very likely to stay depressed or continue declining for the rest of the year. Managers are delaying raising their new funds, trying to stretch out their existing ones, and there is just not a ton of new capital coming into the space. Now macro is a big uncertainty and if rates fall and the economy rebounds and ETH/BTC rip, this could all change over the course of a few quarters. But absent that, I don’t see any short term recovery.

This also potentially makes 2023H2/2024H1 a great time to invest. If last cycle is any indication, the best time to deploy capital was early 2019 to early 2020. I believe we’re seeing some of this play out again. Deals are less competitive, funds have longer to diligence deals, and valuations are down meaningfully. 12-18 months ago we were seeing crypto seed deals getting done at $25-35M equity valuations (with many a lot higher) and very little happening in pre-seed. We’re now seeing teams raise pre-seed rounds at $5-12M valuations and seed rounds at $10-20M valuations.

We’re open for business and aiming to invest aggressively through this downturn. We deployed more capital last quarter than we did in the preceding eight months. We launched Lattice because we believed partnering with crypto founders from day one was a generational opportunity. And we’ve never had higher conviction in that.

This is not legal or financial advice.

Some of my fundraising data does not line up across sources - the Pitchbook data and Messari fundraising data don’t always agree. I think the Messari data is more comprehensive, but it does not extend back to last cycle. CB Insights data generally supports the Pitchbbook data.